US stocks experience largest drop in 10 weeks

Market Summary

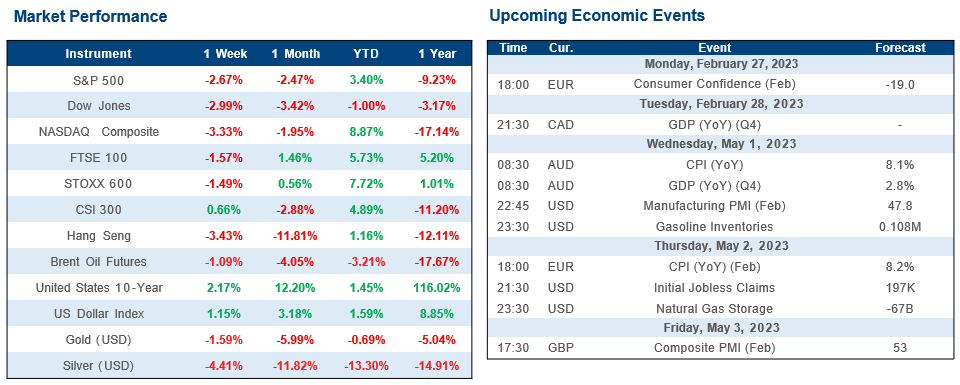

Last week, investors focused on the decline in U.S. stocks and high inflation in the United States.

In the United States, stocks suffer biggest decline in 10 weeks. At its close on last Friday, the S&P 500 index had surrendered roughly 35% of the rally that began in October. The core personal consumption expenditures (PCE) price index jumped 0.6% in January, above expectations of an increase of 0.4%. The yield on the benchmark 10-year U.S. Treasury note nearing 4.00% for the first time since mid-November. In Europe, shares fell. In local currency terms, the pan-European STOXX Europe 600 Index ended 1.42% lower. Inflation in the Eurozone eased in January to an annual rate of 8.6% from 9.2% the previous month. However, the core inflation measure—which excludes fuel and food prices—accelerating to 5.3% from the 5.2% registered in December. The composite Purchasing Managers' Index (PMI) in the Eurozone rose to 52.3 in February from 50.3 in January.

In Asia, equities in Japan lost ground over the week. Next BoJ Governor emphasizes monetary policy continuity. Flash PMI data showed sustained growth in Japan’s services sector in February. However, the health of the manufacturing sector deteriorated. Chinese stocks advanced after three weeks of losses. The Shanghai Stock Exchange Index gained 1.34% and the blue-chip CSI 300 added 0.66% in local currency terms. China’s yuan currency dropped to a seven-week low against the dollar.

Major News

The Chinese foreign ministry on last Friday released a 12-point paper, “Dialogue and negotiation are the only viable solution to the Ukraine crisis,” the foreign ministry said in the document.

Joe Biden has said he did not think China would send weapons to Russia to help its military campaign in Ukraine, but he warned that he “would respond” if Beijing did so.

KPMG is cutting nearly 700 jobs in its US advisory business and about 200 in Australia. Meanwhile, McKinsey will make up to 2,000 of its 45,000 people redundant as part of a global restructuring following years of rapid expansion.

German economy shrank 0.4% in fourth quarter, raising doubts over the ability of Europe’s biggest economy to escape recession and recover swiftly from its energy crisis.

What Caught Our Attention

China emerged as a big overseas lender with astonishing speed. Today it is a larger creditor than either the IMF or the World Bank. This largesse was a boon for poorer places seeking to finance infrastructure projects. But as borrowers have hit trouble, it has become a complication. Zambia and Sri Lanka are mired in debt-restructuring talks with Chinese and other creditors. They may soon be joined by Pakistan.

In addition, loans have accordingly shrunk in value. In 2016 new commitments to sovereigns and state-backed entities made by China’s two big “policy banks” were twice as large as those of the World Bank, reckon researchers at Boston University. In 2021 China’s two banks promised less than a tenth as much.

Moreover, China’s existing stock of loans could also still hit trouble. The fear of losing access to Chinese finance is one reason why poor countries have been slow to ask for forgiveness on their debts. But if future Chinese finance is no longer on offer, requests for debt restructuring may rise, because borrowers know that they have less to lose.

Source: Kredens Capital, T. Rowe Price, Bloomberg, Financial Times, Wall Street Journal, The Economist, Nikkei Asia